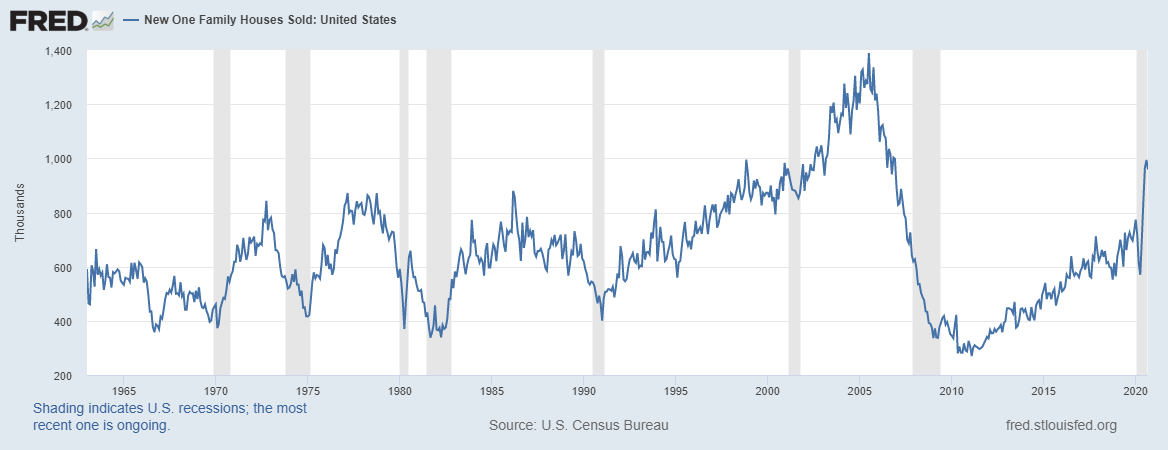

The one economic sector that has blown away my estimates this year has been the new home sales market. I predicted peak year-to-date growth of 4.7% but this was before COVID-19, which temporarily crushed bond yields and mortgage rates.

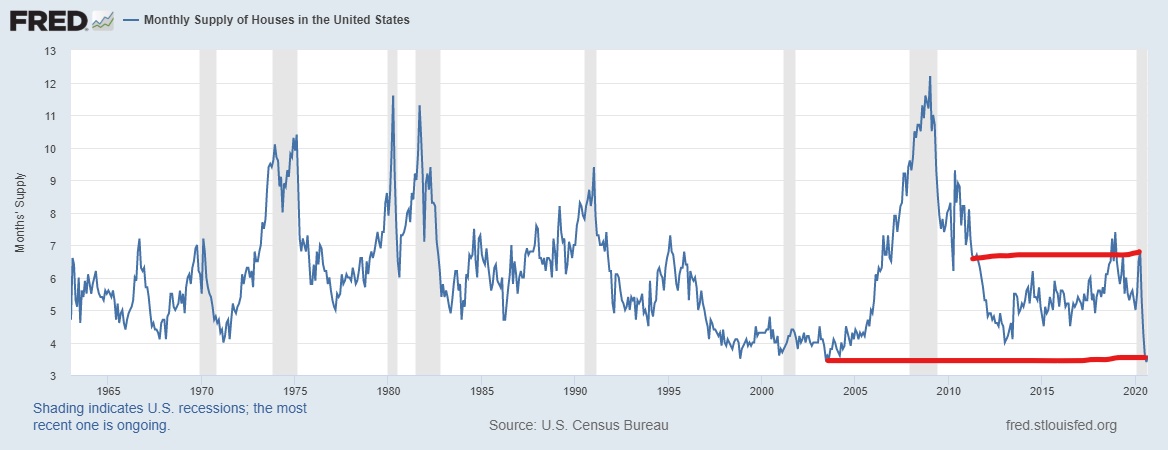

This sector is very sensitive to yields in both a positive and negative direction. When mortgage rates got to 4.75% -5% in 2018, demand fell and inventory for new homes went up. This dramatically slowed the rate of growth in construction in 2019. We had to work off the excess housing supply created with those higher rates to get housing starts to be roughly flat for 2019. But, this isn’t what happened this year when mortgage rates went below 3%.

Today new home sales are up 32.1% year over year and are up 16.9% year to date. Details from the Census Bureau/HUD report released today:

- Sales of new single-family houses in September 2020 were at a seasonally adjusted annual rate of 959,000. This is 3.5% below the revised August rate of 994,000, but is 32.1% above the September 2019 estimate of 726,000.

- The median sales price of new houses sold in September 2020 was $326,800. The average sales price was $405,400.

- The seasonally adjusted estimate of new houses for sale at the end of September was 284,000. This represents a supply of 3.6 months at the current sales rate.

When tracking new home sales data, it is important to note if the revisions confirm the trend. The data in this sector can show wild month-to-month swings that are usually corrected back to the trend line — so don’t put too much faith in big negative or positive prints.

How servicers can prepare for potential default wave

Sutherland Mortgage Services President Krish Swaminathan discusses the next wave of servicing, how servicers can best communicate with their customers and the technology available to help with compliance, even in a work-from-home environment.

Presented by: Sutherland

If you follow me on Twitter you know I have urged caution with the recent parabolic move in the new homes sales data. Having said that, even with the negative revisions and the missed sales report, this data line still looks too hot to me. So, expect some moderation but the story is legit: the new home sales sector is having its best in many years.

The previous two-month revisions came in higher than I anticipated, so this report beats my expectation. The last three months of sales have been amazing for me to watch. As the housing 2020 V-shape recovery man who has been pushing a year 2020-2024 housing theme for many years, this year’s data is much stronger than I could ever have imagined.

July 965,000

August 994,000

September 959,000

In my opinion, the monthly supply chart for the new home sales is the most important chart to follow in housing. As a rule of thumb you don’t want monthly supply to go above 6.5 months. When this happens housing construction stalls. This is what happened in 2018 and this year in the month of April at 6.8 months. Today, however, inventory looks excellent, standing at 3.6 months.

Anytime inventory dips below 4.3 months is great in my book because that is where supply should be for the new home sales sector post-1996. I like to use post-1996 housing data for comparison because this was the period when mortgage rates went much lower and changed the landscape for the monthly supply data. When we get monthly supply data to 4.4 to 6.4 months, this says demand is not booming but good enough for housing starts to grow single-family construction. And that is what we like to see because the new home sales market drives residential construction.

Link to Article